When it comes to buying a home, most people are familiar with the essentials of a mortgage. You know you need to secure money from a lender, pay interest, and make monthly payments until the loan is settled. However, the true cost of a mortgage involves much more than just those traditional components. Understanding your real mortgage costs is vital for making wise financial decisions that will impact your budget and overall financial health.

To fully grasp the financial commitment of a mortgage, you need to consider a multitude of factors that go beyond the principal and interest. These comprise property taxes, homeowners insurance, private mortgage insurance, and even prospective homeowners association fees. Using a mortgage calculator can assist you break down these costs and provide a better picture of what you will be spending each month. With the right tools and information, you can navigate the nuances of mortgage costs and make a choice that aligns with your financial goals.

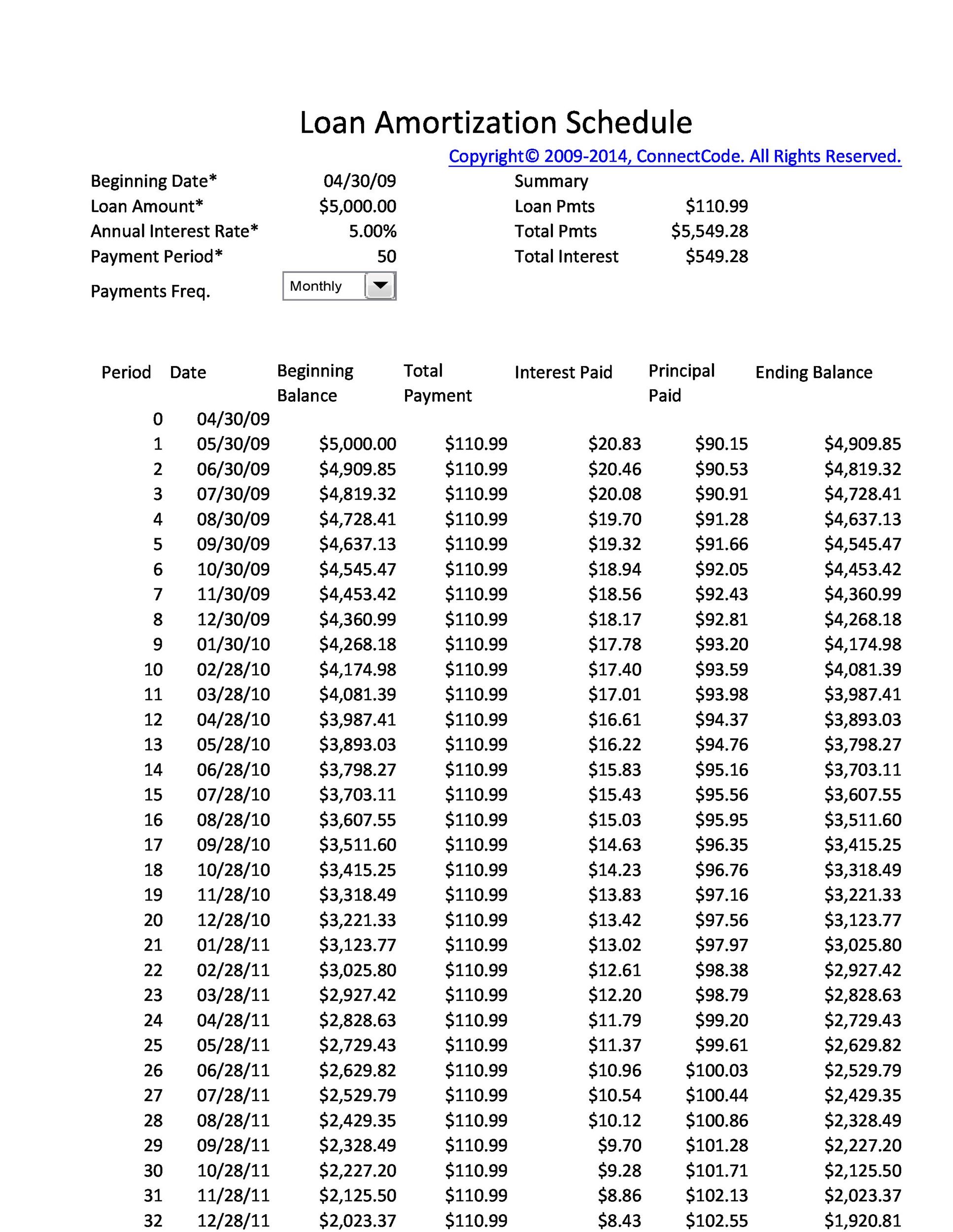

Grasping Home Loan Estimators

Home loan calculators are crucial tools that help potential homebuyers estimate their monthly mortgage payments. By entering important details like the loan amount, APR, and mortgage term, users can quickly achieve insight into what their financial commitment will entail. These calculators can accommodate various situations, allowing users to adjust variables such as initial payment and property taxes to get a better picture of their possible expenses.

One of the primary benefits of using a home loan calculator is its ability to provide a summary of the loan costs over time. Users can see how much of their monthly payment is allocated to loan balance and interest compared to property taxes, homeowner's insurance, and PMI if applicable. This breakdown helps in understanding how the mortgage evolves as payments are made and how interest grows throughout the loan term.

Additionally, many web-based home loan calculators offer advanced features that allow users to examine different loan scenarios. Homebuyers can experiment with different interest rates and loan terms to see how these variations affect their regular payments and overall costs. This flexibility enables users to make more educated decisions about their mortgage options and to select a mortgage that fits their economic objectives.

Unseen Expenses in Mortgages

When determining the true cost of a mortgage, it's essential to go above the principal and interest payments. Numerous homebuyers ignore multiple undisclosed costs that can greatly affect their financial responsibilities. These can include property taxes, homeowner’s protection, and private mortgage insurance, which are often rolled into monthly payments but can accumulate over time. Grasping these factors is key for getting an correct understanding of the total financial outlay involved in having a house.

Final fees are yet another hidden charge that can surprise many borrowers. These costs can range from loan origination charges and appraisal costs to title insurance and lawyer fees, generally totaling two to five percent of the property cost. It's crucial to be mindful of these charges as they can considerably boost the total needed at closing when closing the transaction. Numerous homebuyers may only focus on the down payment, ignoring to account for these key costs.

Finally, ongoing upkeep and repair expenses are often overlooked. Homeownership comes with the responsibility of keeping the home in good state, which includes regular maintenance, unexpected repairs, and potential HOA fees. These costs can vary widely but can pile up swiftly, making it important to factor them into your overall mortgage estimates. HipoteCalc of these concealed fees will help homebuyers plan better and stay clear of financial surprises down the line.

Crafting Informed Choices

Understanding the true expenses of your home loan is crucial for making informed financial decisions. Many buyers emphasize exclusively on the periodic installment, but it's critical to factor in the entire economic picture. Elements such as interest rates, financing terms, property payments, homeowner's protection, and PMI can greatly impact your comprehensive costs. A holistic view allows you to evaluate whether you can truly finance the property and how it fits into your long-term monetary aspirations.

Employing a mortgage calculator can assist you uncover these concealed charges. By entering parameters such as loan amount, rate rate, and term period, you can receive a better insight of your anticipated payments. A few complex calculators even consider in additional expenses like taxes and insurance, providing a clearer monthly payment calculation. This tool enables you to play with different options to see how modifications might influence your financial resources.

Once you have a solid grasp of your actual mortgage costs, you’re well prepared to negotiate terms and look for the most favorable offers. Keeping all these elements in mind helps you avoid typical traps, such as stretching your financial limits or underestimating future obligations. Being well-informed positions you to take decisions that conform with your monetary health and homeownership goals.